Boost Your Credit Score: A 6-Month Guide to a 50-Point Increase

Understanding Your Personal Credit Score: How to Improve It by 50 Points in 6 Months involves strategic actions like correcting errors on your credit report, lowering your credit utilization ratio, and making timely payments to demonstrate responsible credit behavior, potentially leading to a significant score increase.

Are you looking to enhance your financial health? Understanding Your Personal Credit Score: How to Improve It by 50 Points in 6 Months can seem daunting, but with a focused strategy, it’s achievable. Let’s explore practical steps to boost your creditworthiness.

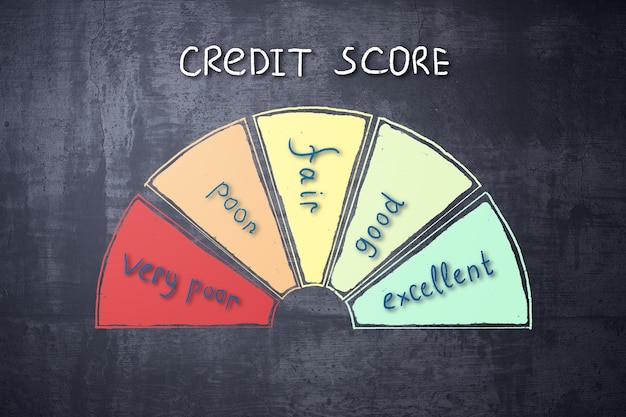

Understanding Your Credit Score: The Foundation

Your credit score is more than just a number; it’s a key indicator of your financial trustworthiness. It affects your ability to secure loans, rent an apartment, and even get certain jobs. Before diving into improvement strategies, it’s crucial to understand what influences your credit score.

Several factors contribute to your credit score, each carrying different weight. Payment history, credit utilization, credit age, credit mix, and new credit accounts all play a role. Let’s break down each of these components.

Key Factors Influencing Your Credit Score

- Payment History: This is the most significant factor, representing about 35% of your score. It reflects whether you pay your bills on time.

- Credit Utilization: This refers to the amount of credit you’re using compared to your total available credit, ideally kept below 30%.

- Credit Age: The length of time you’ve had credit accounts open also matters. A longer credit history can positively impact your score.

Understanding these elements is the first step toward taking control of your credit score. Now let’s look into developing a strategic plan to leverage these factors to your advantage.

In summary, understanding the various factors that impact your credit score is paramount for effective improvement. By focusing on key areas such as payment history, credit utilization, and credit age, you can start building a solid foundation for a better credit profile.

Step 1: Obtain and Review Your Credit Report

The first concrete step in improving your credit score is to access and thoroughly review your credit report. You can obtain a free copy from each of the three major credit bureaus—Equifax, Experian, and TransUnion—annually through AnnualCreditReport.com.

This report contains valuable information about your credit history, including your payment behavior and outstanding debts. Identifying and correcting errors in your credit report is a crucial first step to ensure an accurate reflection of your financial responsibility.

How to Dispute Errors on Your Credit Report

- Identify Inaccuracies: Carefully review each section of your credit report for any errors like incorrect balances, late payments inaccurately reported, or accounts that don’t belong to you.

- Gather Documentation: Collect any documents that support your claim, such as bank statements, payment confirmations, or letters from creditors.

- Submit Disputes: File a dispute with each credit bureau that has the error listed on your report. Use certified mail for documentation.

Correcting errors can lead to an immediate boost in your credit score, especially if the inaccuracies are significant. This foundational step ensures that your credit improvement efforts are based on accurate information. Now let’s dive into building a budget.

To conclude, the initial step of obtaining and reviewing your credit report is vital for identifying and addressing any inaccuracies that might be negatively affecting your credit score. By taking proactive measures to correct these errors, you set a clear path for credit score improvement.

Step 2: Create a Budget and Pay Bills on Time

Consistently paying your bills on time is arguably the most effective way to improve your credit score. Payment history makes up a substantial portion of your credit score, so demonstrating reliable payment behavior can significantly boost your score.

Creating a budget is an essential tool for managing your finances and ensuring timely bill payments. A well-structured budget helps you track your income and expenses, allowing you to allocate sufficient funds for each bill.

Tips for Creating an Effective Budget

- Track Your Income: Identify all sources of income you receive regularly.

- List Your Expenses: Categorize your expenses into essentials (rent, utilities) versus non-essentials (entertainment, dining out).

- Set Financial Goals: Establish clear financial goals, such as paying off debt or saving for a down payment.

By having a robust budget, you will have enough money to pay you bill on time. This shows that you are financially responsible. Let’s explore the next step.

In conclusion, structuring an effective budget and making timely payments are crucial steps toward improving your credit score. By effectively managing your finances and demonstrating reliable payment behavior, you can significantly enhance your credit profile and overall financial health.

Step 3: Reduce Your Credit Utilization Ratio

Your credit utilization ratio, or the amount of credit you’re using compared to your total available credit, is another crucial factor in your credit score. Experts recommend keeping this ratio below 30% to avoid negatively impacting your credit score.

High credit utilization can signal to lenders that you are over-reliant on credit, which can lower your creditworthiness. Conversely, maintaining a low credit utilization ratio demonstrates responsible credit management.

Strategies to Lower Your Credit Utilization

- Pay Down Balances: Make extra payments to reduce your credit card balances.

- Request a Credit Limit Increase: Increasing your credit limit can lower your utilization ratio without increasing your spending.

- Open a New Credit Card: Opening a new credit card can increase your overall available credit, potentially lowering your utilization ratio.

Reducing your credit utilization ratio is a proactive step that can lead to significant improvements in your credit score. By keeping your balances low and managing your credit responsibly, you can demonstrate financial prudence to lenders.

In summary, a lower credit utilization ratio signals to creditors that you are managing your credit responsibly, which can greatly improve your credit score. Prioritize strategies to keep your credit utilization below 30% to see positive effects on your score.

Step 4: Avoid Opening Too Many New Accounts

While opening a new credit card can sometimes lower your credit utilization ratio, it’s important to avoid opening too many new accounts in a short period. Each new credit application results in a hard inquiry on your credit report, which can slightly lower your score.

Too many inquiries can signal to lenders that you are actively seeking credit, which can be seen as risky behavior. Therefore, be mindful of how many new accounts you apply for and spread out your credit applications over time.

Tips for Managing New Credit Accounts

- Space Out Applications: Avoid applying for multiple credit cards or loans at the same time. Spread them out over several months.

- Limit Inquiries: Be selective about which offers you apply for, focusing on those that align with your financial goals.

- Monitor Your Credit: Keep an eye on your credit report to detect any unauthorized inquiries or suspicious activity.

In conclusion, managing new credit accounts effectively is about striking a balance between leveraging credit opportunities from new cards like rewards to avoid over extending yourself. Doing those will keep your credit score doing well.

In summary, being strategic about opening new credit accounts and managing your credit inquiries can help maintain a healthy credit score. Avoid unnecessary applications and monitor your credit report regularly to prevent any negative impacts.

Step 5: Keep Old Credit Accounts Open

The age of your credit accounts is another factor that influences your credit score. Keeping older credit accounts open, even if you don’t use them, can positively impact your credit score by demonstrating a longer credit history.

Closing old accounts can shorten your credit history and reduce your overall available credit, potentially increasing your credit utilization ratio. Therefore, consider keeping these accounts open and making occasional small purchases to keep them active.

Benefits of Keeping Old Accounts Open

- Longer Credit History: A longer credit history shows lenders that you have experience managing credit over time.

- Higher Available Credit: Keeping old accounts open maintains a higher overall credit limit, which can lower your credit utilization ratio.

- Positive Impact on Credit Mix: A mix of different types of credit accounts can also benefit your credit score.

Keeping old credit accounts open is a simple yet effective way to boost your credit score over time. By maintaining a longer credit history and a higher overall credit limit, you can improve your creditworthiness.

In conclusion, maintaining older credit accounts demonstrates a longer history of managing credit, which can positively influence your credit score. Even if you don’t use these accounts regularly, consider keeping them open to enhance your credit profile.

| Key Point | Brief Description |

|---|---|

| ✅ Check Credit Report | Find errors and fix them to ensure accurate info. |

| 🗓️ Pay Bills on Time | Consistent, timely payments show responsibility. |

| 💰 Lower Credit Use | Keep balances below 30% of your credit limit. |

| 💳 Keep Old Accounts | Older accounts show a longer, stable credit history. |

FAQ

▼

You should check your credit report at least once a year. It’s wise to space out checks among the three major credit bureaus to monitor regularly.

▼

A good credit utilization ratio is below 30%. Keeping it lower can improve your credit score.

▼

Credit score improvements can vary. Consistent positive habits can show within a few months, but significant changes may take six months or longer.

▼

If you find an error, dispute it with the credit bureau and provide documentation. They are legally obligated to investigate and correct.

▼

Closing a credit card can potentially hurt your credit score, especially if it reduces your overall available credit or shortens your credit history.

Conclusion

Improving your credit score by 50 points in 6 months is an achievable goal with consistent effort and a strategic approach. By understanding the factors that impact your credit score, correcting errors, paying bills on time, lowering your credit utilization ratio, and managing your credit accounts responsibly, you can enhance your creditworthiness and unlock better financial opportunities.